ECONOMYNEXT – Sri Lanka’s bank interest rates have continued to edge up after a rate cut in May 2025, amid a strong economic recovery made possible by the stability provided by the central bank through past deflationary policy as well as stable government policies.

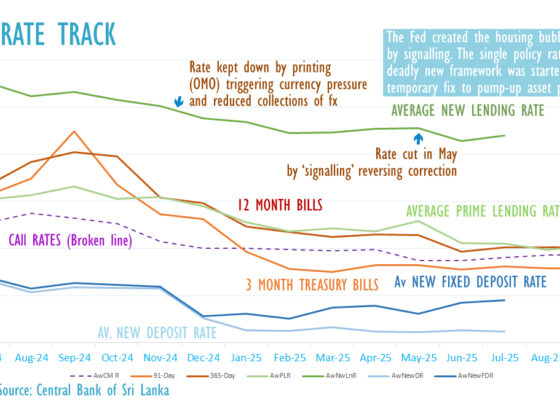

According to central bank data the weighted average new fixed deposit rate fell to 6.62 percent in May and climbed to 6.85 percent in June and 6.90 percent in July.

However, banks are now mobilizing 12-month deposits at 7.75 percent and above to finance strong credit demand and an economic recovery.

The economic recovery may also have been helped by reduced government capex, which reduced domestic state borrowings and allowed private citizens to deploy resources to the most productive areas, bringing compounded long-term growth rather than bureaucratic spending.

The weighted average new lending rate climbed to 10.56 percent in April from 10.46 percent in March, fell to 10.28 percent in June, a month after the rate cut.

It has picked up to 10.40 percent by July.

At the moment the central bank is not printing money in large scale like in the last quarter of 2024, and banks are covering shortfalls at the standing lending rate at 8.25 percent encouraging banks to raise deposits or curtail lending until loan repayments or deposits came.

The treasury bill yields are now bunched together and almost fixed for a long period in a straight line in what analysts have previously called a ‘ramrod rate anomaly.’

Such ‘ramrod’ rate anomalies have usually preceded currency crises and steep rate hikes late when they were enforced by inflationary open market operations and what is called ‘direct market operations’ in Sri Lanka.

At the moment the central bank is not printing money through aggressive open market operations, though concerns have been raised about inflationary swaps, but the call money rates are suppressed through a signalled ‘mid-corridor’.

A true single policy rate however requires large volumes of excess liquidity which will also result in a fairly quick default from forex shortages, loss of confidence.

There has been some moral suasion from time to time, according to market participants, to keep rates down.

Take up of bills have been erratic and it is not clear whether bill yields are being kept down to conform to the single policy rate, so -called. But banks have reduced their holdings of bills in line with past practices when rates were cut during a credit upturn.

In the past macro-economists have squeezed funding to the government by suppressing rates using powers in the monetary law including open market operations and then falsely blamed deficits for inflation and currency collapses, though interest rate controls were actually blocking the roll-over of past deficits.

However, since the Treasury bill sales were in the control of the central bank and not the Treasury, politicians were unaware of the real sources of inflation.

In the case of the Fed – Treasury Accord that led to the so-called ‘independence’ of the Fed, it was freed from the need to conduct open market operations with long bonds (Liberty Bonds of World War I) though macro-economists later falsely blamed it on the Korean War.

In fact, in 1951, the US ran a budget surplus and Congress denied the full tax increases sought for by President Truman for a second time.

The inflation during the Korean war did not come from deficit financing (in 1950 President Truman and Secretary Snyder who put pressure on the Fed to defend the rate of Liberty Bonds to protect war widows) sought for and got one tax increase saying it would help inflation.

However macro-economists have continued to blame the Korean war (implied deficits) for the inflation, though Marriner Eccles, in seeking the return to a ‘bills only’ policy pointed out that it was open market operations that was the culprit.

“There is going to be nothing for us to protect in this country unless we are willing to do what is necessary to protect the dollar,” Fed Governor Marriner Eccles, a classical economist in the style of 19 the century greats such as David Ricardo who had logical reasoning powers is quoted as saying in Fed minutes.

“Our responsibility is not a minor one; it is a very great one under the conditions that exist, and if we fail, history will record that we were responsible, at least to a very great measure, in bringing about the destruction or defeat of the very system that our defense effort is being made to protect and defend.

“We are not in a war. We do not now have deficit financing.

“You only protect the public credit by maintaining confidence in the Government and in its securities and to the extent the public will buy and hold those securities. The thing we are doing is to make it possible for the public to convert Government securities into money and to expand the money supply of this country by $7 billion in six months.”

“We are almost solely responsible for this inflation…the whole question of having rationing and price controls is due to the fact that we have this monetary inflation, and this Committee is the only agency in existence that can curb and stop the growth of money.

He pointed out that inflation had started just before the Korean war began, with a strong expansion in credit finance by open market operations.

Sri Lanka is not doing open market operations yet, though macro-economists have got themselves the legal power to do so by midnight gazette, under Sri Lanka’s controversial new monetary law backed by the International Monetary Fund.

Countries end up with generally higher interest rates due to the monetary debasement, which destroy capital, though factors like wealth tax and progressive taxes can also prevent savings being generated by the most productive citizens.

Countries with strong currencies and run deflationary policy in some cases, generally have very low interest rates.

If rates are allowed to go up from time to time, and monetary stability is maintained, Sri Lanka’s interest rates could go back to pre-central bank levels or close to that given the inflationism in the US.

Sri Lanka also had low interest comparable to developed nations when the central bank was created and 20-year bonds were sold at 3 percent and short-term ones at 1.5 percent.

In 2025, bond sales are going out of the hands of the central bank to the Treasury, however since the debt office officials are trained by the central bank, questionable practices such as the buffer strategy or the current problem with bills could continue to take place.

However at least the government is raining money through bonds, though at higher rates.

What macro-economists have achieved in pushing up rates and destroying the currency with ‘rate cuts’ and similar action is remarkable, analysts say.

However ultimately it is the fault of the parliament for giving power to macroeconomists to play with the money of the people to satisfy their inflationist desires or doctrines based on fads coming from US universities in particular.

The world is now suffering a severe rejection of economics by the Western central banks and those who advocate them with both stimulus and the single policy rate having destroyed government finances. (Colombo/Sept22/2025)